Soybean Markets – Turning of the Tide?

Written for Sevita by Kendra Dauer, Risk Management Consultant, FCM Division of StoneX Financial Inc.

The Tide

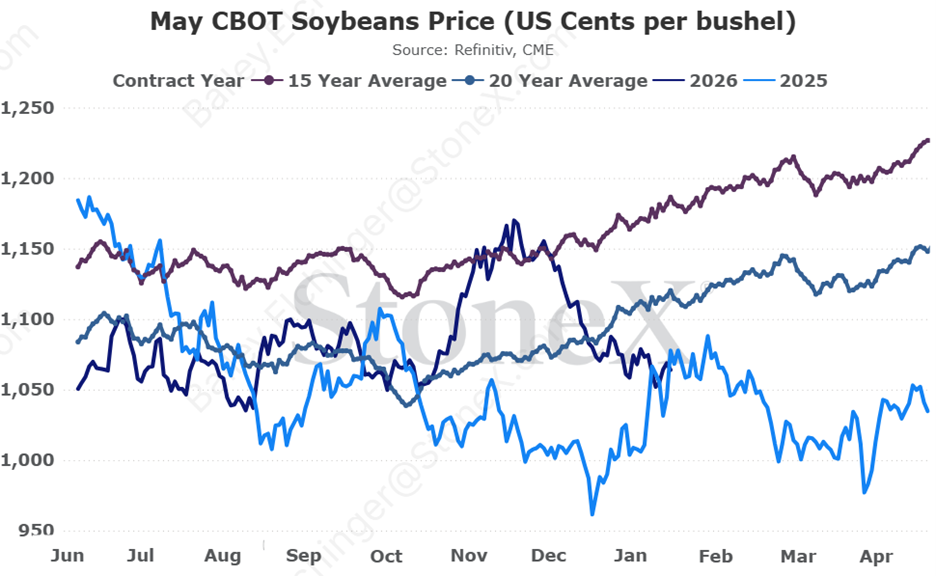

Following the price decline in December, the soybean market seemed to find some footing through the flip of the calendar. New reports that China was beginning to auction off state reserves – this would make room for China’s new soybean purchases from the U.S. and in the market’s eyes ‘new demand.’ Using the quotations is intentional because, as we know, the USDA had already plugged in China demand into the balance sheet. And with their nonexistent purchases in the first half of the marketing year, the ‘commitments’ they made to purchase soybeans – in reality are just playing catch-up for demand the USDA was already expecting. Nonetheless, this changed the tide for the market as it found steadier waters ahead of the USDA report.

The Turn

The USDA released its January WASDE and Stocks report earlier this month – turning the market back to multi-month lows. The December 1 soybean stocks were estimated up 190 million bushels versus last year – with most of those stocks also sitting in the Western Corn Belt. Breaking down the balance sheet changes, the USDA elected to leave bean yields unchanged at 53 bushels per acre, when the market widely anticipated a reduction in yield, which is a record yield by 0.9 bushels per acre. With the slight increase to planted and harvested acres, production was seen up a touch from last month – but still an overall smaller production number versus the 24/25 crop. On the demand side of the balance sheet, there was a reduction to exports – which is justified due to our slow shipment pace thus far. Overall net changes increased bean carryout by 60 mbu to put ending stocks at 350 mbu. No matter which way I paint it, that large of a carryout number does not lead me to be bullish on the soybean market.

High Tide? Low Tide?

So, knowing all of this, what troubled waters lay ahead? Good news, after the initial reaction lowered, following the report, the soybean market seemed to have found a ‘bottom’ to the market. We continue to see purchases from China, again – this is demand that we already knew was going to happen, but it is positive reinforcement for the market. How deep is China’s demand? Sales data shows that China has met their 12 mmt purchase commitment as of last week. Brazil’s soybean crop harvest has started, one has to think that China pauses their U.S. purchases for now, to opt for cheaper South American supplies. Where do we go from here? The soybean market continues to lack a fundamentally driving story. Given the recent price action, we have seen in the market and the sort of ‘bottoming out’ that we saw last week, I would anticipate for the market to be comfortable in its sideways pattern until we get closer to the growing season.

It feels like steady waters ahead for the soybean market, until a new story comes along to cause ripples. The stormy seas we have experienced over the last six months should make for more confident sailors (producers and consumers). Both sellers and buyers have seen wide swings in the marketplace and know that having price targets in mind and orders working is the best practice.

Recent Articles

-

//Market Report

//Market ReportOn the Move Again

Where we’ve been- Since harvest, soybeans have seen their share of ups and downs in the market. From the tariff war getting resolved in November, to the surprises in the January stocks report – soybeans had been stuck in a trading range for several months even if it was a large range.

read more -

//Market Report

//Market ReportRockets Away

Since the writing of the comments in January the front-month bean contract has rallied nearly a dollar. As we mentioned in last month’s comments the tides seemed to have turned in the month of January as we saw China finally beginning to full fill some of their purchase agreements and shipments of beans begin to occur. Additionally, we saw the January supply/demand report from the USDA. As those tides turned we also so more conversations between U.S. President Trump and

read more -

//Market Report

//Market ReportBuy the Rumour, Sell the Fact

Last month’s comments started out talking about a significant gap on the January bean chart that occurred at the end of October and set the market up for a rally throughout the month of November. That rally was largely due to the belief that China would be buying ‘significant’ amounts of U.S. soybeans. This belief was fueled by numerous meetings and ‘anno

read more

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized; regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2022 StoneX Group Inc. All Rights Reserved.